Apple has found itself at the top of the list of the world’s leading smartphone vendors and Apple is the became the largest smartphone vendor in terms of revenue and profits during the second quarter of 2011. Apple recently topped another list as well as it was named the number one maker for smartphones in June within the United States and IDC said the feature phone forecast isn’t expected to be any rosier in the future and the shipment growth of feature phones won ‘t exceed 1.1 percent in the coming years……………….

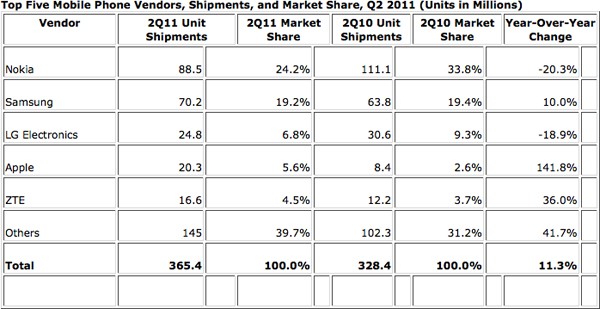

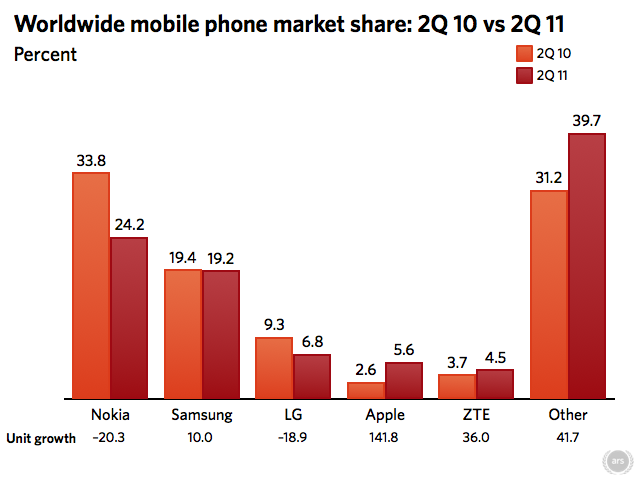

The worldwide mobile phone market grew 11.3% year over year in the second quarter of 2011 (2Q11), despite a weaker feature phone market, which declined for the first time since 3Q09. According to the International Data Corporation (IDC) Worldwide Mobile Phone Tracker, vendors shipped 365.4 million units in 2Q11 compared to 328.4 million units in the second quarter of 2010. The 11.3% growth was lower than IDC’s forecast of 13.3% for the quarter and was also below the 16.8% growth in 1Q11. The feature phone market shrank 4% in 2Q11 when compared to 2Q10. The decline in shipments was most prominent in economically mature regions, such as the United States, Japan, and Western Europe, as users rapidly transition to smartphones. This was the first decline since Q3 2009 and reflected a combination of conservative spending and continued shift to smartphones. “The shrinking feature phone market is having the greatest impact on some of the world’s largest suppliers of mobile phones,” said Kevin Restivo, senior research analyst with IDC’s Worldwide Mobile Phone Tracker. “Stalwarts such as Nokia are losing share in the feature phone category to low-cost suppliers such as Micromax, TCL-Alcatel, and Huawei.””For the overall market to grow by double digits year over year, despite the decline in feature phones, is testament to the strength of the global smartphone market,” noted Ramon Llamas, senior research analyst with IDC’s Mobile Phone Technology and Trends team. “While this is not a new trend – smartphones have been the primary engine of growth for the last several quarters – it does mark something of a transition point, as demonstrated by the growing number and variety of smartphones featured in the vendors’ portfolios.”

The feature phone forecast isn’t expected to be any rosier in the quarters and years to come. Shipment growth of the device type won’t exceed 1.1% in any year forecasted by IDC. The traditionally slow second quarter in Asia/Pacific was exacerbated by Nokia’s channel inventory corrections in China. Apple thrived in China thanks to strong iPhone 4 demand. As well, a number of domestic brands in Southeast Asia like CSL, Nexian, Q-Mobile and Wellcom grew sales of Android-powered smartphones. China-based vendors gained share in India and Southeast Asia at the low end. In Japan, the impact of the earthquake continued into April and May as component shortages forced manufacturers to release new models in June while customer demand was harder to fulfill. In Western Europe, the market declined sequentially compared to the first quarter. The feature phone market declined while smartphone shipment growth slowed as phone makers and carriers reduced inventories in advance of expected third-quarter product launches. Feature phone dependent suppliers were not able to offset feature phone weakness completely with higher smartphone sales. The CEMA markets performed well on a year-over-year basis despite civil unrest in Egypt and other Arab countries, where sales were negatively impacted as a result. Samsung gained share while Chinese brands continued to make inroads in the region. In North America, smartphones once again took center stage, propelled by lower prices, key device launches, and enhanced channel marketing. In particular, Android-based devices extended their lead in the United States and took leadership in Canada thanks to Samsung, Motorola, HTC and LG. Meanwhile, demand for feature phones continued to slide, but there still existed pockets of interest for voice-centric and quick-messaging devices. Still, as the region heads towards a smartphone-centric future, IDC expects feature phones to represent an increasingly smaller portion of the market.

The Latin America market growth was driven by low-cost smartphones, specifically those with social networking features. Lower smartphone prices, including those of the Android variety, are driving smartphone penetration in several Latin American countries. Price is expected to be a point of differentiation, as well as applications and device features – between Android players in future. Nokia‘s hold on the top global mobile phone spot weakened last quarter as inventory buildups in traditional strongholds, namely China and Europe, led to sharp year-over-year shipment declines. Nokia‘s global feature phone and smartphone businesses suffered a similar fate. One positive sign for Nokia last quarter were dual-SIM devices; the company shipped over 2.6 million of these in the second quarter. Over the long term, Nokia’s smartphone fortunes will be dictated by its ability to sell Windows Phone 7 smartphone devices, which are expected to hit the market this year. It is Nokia’s primary smartphone platform of the future. In the meantime, Nokia is trying to sustain shipment volume with low-cost mobile phones and devices powered by the aging Symbian smartphone platform.

Samsung posted double-digit growth from the same quarter a year ago and just slightly slower growth than the overall pace of the market. Like other vendors it realized a decrease in demand for its feature phones, but made up the difference with continued success for its Android-based Galaxy smartphones. The difference between Samsung and market leader Nokia continued to shrink, with less than 20 million units separating the two vendors, mostly resulting from Nokia‘s struggles in the market. Still, Samsung expects continued growth into the second half, which could put it in closer contention with Nokia. LG Electronics held on to its number three position during the quarter, thanks in part to its Optimus smartphone sales worldwide. However, a combination of factors – including soft demand for its feature phones, slow pace of smartphone releases, and competitive pressures, led the company to downgrade its outlook for the year by 24%. Originally, LG had anticipated flat growth in 2011 from 2010 levels, even as it expected the overall market to increase by 8%. Should LG’s volumes decrease as much as it anticipates, other vendors may jockey for position ahead of LG.

Apple maintained its number four position overall but closed the gap on Top 5 competitors thanks to another record unit shipment quarter. The company easily posted the highest growth rate of the worldwide leaders despite the fact that its flagship iPhone 4 is now more than a year old. The triple-digit shipment volume growth allowed Apple to more than double its share when compared to the same quarter last year. Apple‘s ability to bring its smartphone momentum to developing economies, where it’s less successful, will help dictate the company’s smartphone fortunes in future. ZTE likewise improved volumes and picked up market share during the quarter, enough to maintain the number five position. Long known as a purveyor of simple, voice-centric mobile phones, ZTE has stepped up its smartphone game with the continued success of its Android-powered Blade and Racer smartphones while announcing Libra, Skate and Amigo smartphones for release in the second half of this year. Feature phones continued to be popular for ZTE with the release of its 547i, a social networking-centric device in Europe.

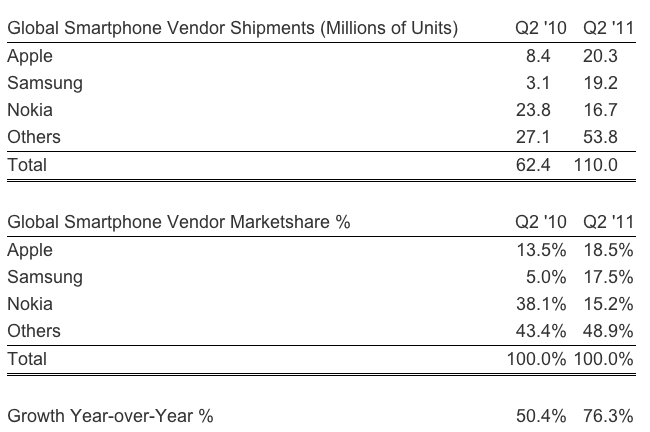

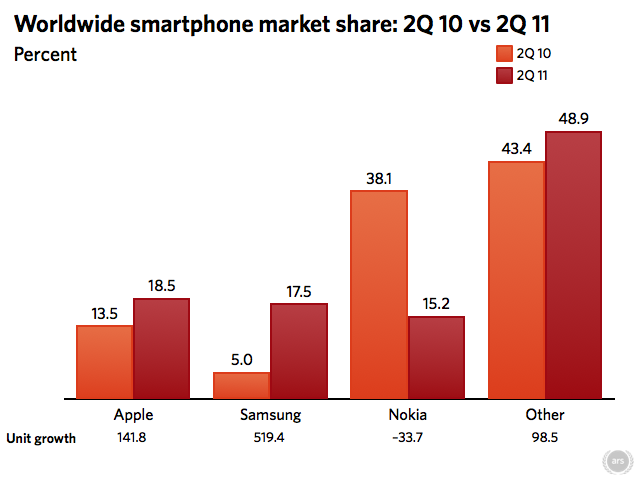

According to the latest research from Strategy Analytics, global smartphone shipments grew an impressive 76 percent annually to reach a record 110 million units in the second quarter of 2011. Both Apple and Samsung overtook long-time volume leader Nokia for the top two spots in our rankings. Alex Spektor, Senior Analyst at Strategy Analytics, said, “Global smartphone shipments grew a healthy 76 percent annually to reach a record 110 million units in Q2 2011. We had previously reported on Apple becoming the largest smartphone vendor in terms of revenue and profits. Now, just four years after the release of the original iPhone, Apple has become the world’s largest smartphone vendor by volume with 18 percent market share. Apple’s growth remained strong as it expanded distribution worldwide, particularly in China and Asia.” Neil Mawston, Director at Strategy Analytics, added, “Samsung overtook Nokia to become the world’s second largest smartphone vendor in Q2 2011. Samsung’s shipments grew a huge 520 percent annually, for 17 percent global smartphone market share. Samsung’s Galaxy portfolio has proven popular, especially the high-tier S2 Android model.” Tom Kang, Director at Strategy Analytics, added, “Having become the first ever vendor to ship 100 million smartphones in a single year during 2010, long-time leader Nokia has slipped two places in our rankings in Q2 2011. The vendor’s 15 percent global smartphone market share is less than half of what it was just one year earlier, as the industry awaits Nokia’s pending transition to Windows Phone 7.”

[ttjad keyword=”iphone”]